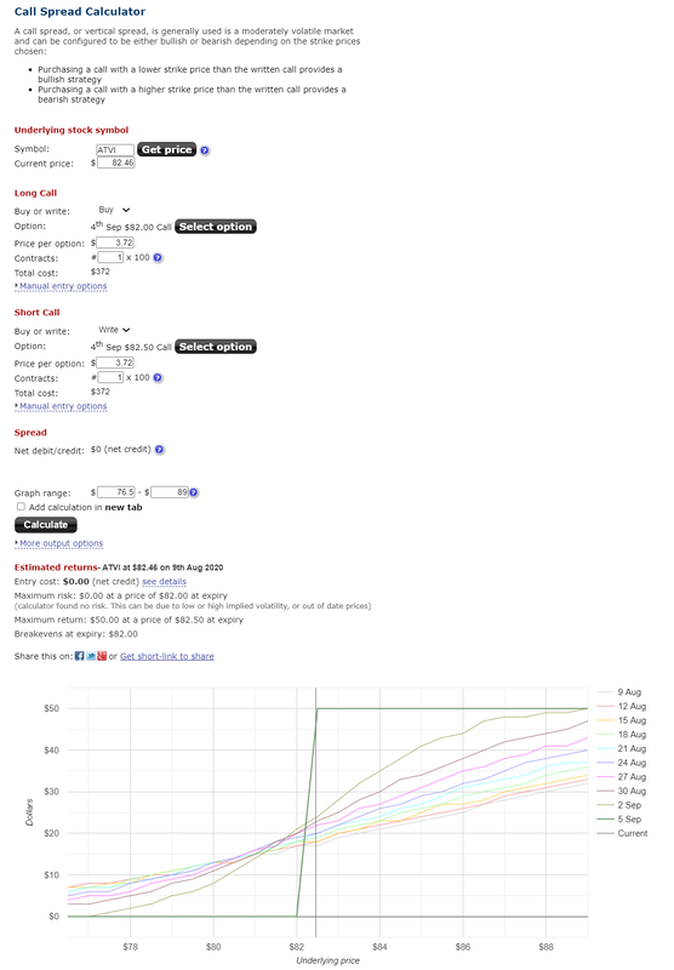

We are building off of our previous post on the ticker symbol 'ATVI' or Activision Blizzard, which had a stock price of $82.46 on August 7th, 2020. Now, Investment Lab has functionality to graph opportunities for options, like we showed you on determining when an option is overpriced . What we do next, is check for inefficiencies of pricing within options. If we perform a credit spread trading strategy, where we sell a call option with the strike price of $82.50 on August 7th at $3.72, and we also buy a call option at $82.00 for $3.72 on August 7th - we would have a risk free trade, meaning if the price of ATVI is less than or equal to $82.00 we lose $0 dollars (see the last image for more detail).

*Note due to transaction costs and slippage (With regard to futures contracts as well as other financial instruments, slippage is the difference between where the computer signaled entry and exit for a trade and where actual clients, with actual money, entered and exited the market using the computer’s signals) we would likely only lose $5-$10 dollars. Lastly, we based the pricing off of the mid price from the bid and ask of Activision Blizzard options.

So to summarize, we risk $5-$10 dollars to make $50 dollars if Activision Blizzards stock price is greater than 82.50 on September 4th. Our software was able to pick the best risk/reward scenario for a given option at a given target price!

*Note due to transaction costs and slippage (With regard to futures contracts as well as other financial instruments, slippage is the difference between where the computer signaled entry and exit for a trade and where actual clients, with actual money, entered and exited the market using the computer’s signals) we would likely only lose $5-$10 dollars. Lastly, we based the pricing off of the mid price from the bid and ask of Activision Blizzard options.

So to summarize, we risk $5-$10 dollars to make $50 dollars if Activision Blizzards stock price is greater than 82.50 on September 4th. Our software was able to pick the best risk/reward scenario for a given option at a given target price!

RSS Feed

RSS Feed